GST compliance is the process of meeting ongoing obligations under the A New Tax System (Goods and Services Tax) Act 1999. It defines how your business charges, reports, and remits the 10% tax to the Australian Taxation Office (ATO).

The process covers registering at the correct turnover threshold, issuing valid tax invoices, claiming input tax credits, and lodging Business Activity Statements (BAS) accurately and on time.

This guide covers the core rules, common mistakes, industry-specific considerations, and implementation steps to help your business maintain full compliance with ATO requirements.

Key Takeaways

GST compliance means accurately charging, reporting, and remitting the 10% tax under the A New Tax System Act 1999. Every Australian business must meet these obligations to avoid ATO penalties.

GST obligations forces businesses with a turnover of $75,000 or more must register for GST, lodge BAS on time, and hold valid tax invoices for all input tax credit claims.

Common mistakes of GST compliance involves misclassifying supplies, relying on invalid tax invoices, and failing to apportion private-use expenses.

Best practices for compliance is to automate tax code assignment, implement e-invoicing, and schedule annual compliance health checks.

What Is GST Compliance?

GST compliance is the mandatory process of meeting all Goods and Services Tax obligations under Australian law. It covers business registration, issuing accurate tax invoices, maintaining financial records, calculating tax liabilities correctly, and lodging returns on time. Compliant businesses can also claim Input Tax Credits (ITC) and avoid ATO penalties.

GST compliance refers to a business’s ongoing adherence to the Goods and Services Tax Act 1999. Since its introduction on 1 July 2000, the GST has turned Australian businesses into tax collectors on behalf of the federal government.

Compliance means identifying taxable supplies, calculating the 10% tax, and claiming input tax credits. It also dictates how invoices are formatted, how long records must be retained, and how transactions are classified within a financial reporting system.

True compliance requires businesses to prove the accuracy of their calculations through comprehensive, accessible documentation.

The compliance landscape evolves constantly. Legislative updates, ATO rulings, and evolving business models require continuous policy reviews.

For businesses of all sizes across Australia, the core principles remain: accuracy, timeliness, and full transparency with the ATO.

Why GST Compliance Matters for Australian Businesses

Non-compliance with GST obligations carries serious risks for any Australian business. The ATO has broad enforcement powers, and the cost of non-compliance consistently outweighs the effort to stay compliant.

1. Financial penalties and interest charges

The ATO can impose administrative penalties for false or misleading statements on a BAS, even when the error is unintentional.

Penalties are calculated as a percentage of the tax shortfall, ranging from 25% for careless errors to 75% for intentional disregard. The General Interest Charge (GIC) accrues daily on unpaid liabilities, compounding a minor shortfall into a significant debt.

2. Increased ATO scrutiny and audits

Late lodgments, unusually high input tax credit claims, or failed data-matching checks can trigger a full ATO audit. Finance teams must divert time from core tasks to gather documentation and respond to auditor queries.

Audits are disruptive and resource-intensive. Engaging external tax professionals to manage an audit can cost tens of thousands of dollars, placing further strain on the business.

3. Reputational and credit risks

Tax non-compliance has consequences beyond ATO penalties. Customers, investors, and business partners scrutinise governance records closely. Lenders review a business’s compliance history when assessing loan applications.

A record of ATO debts or late lodgments can result in higher interest rates or outright rejection of credit applications.

Key GST Obligations Every Australian Business Must Know

Understanding your core GST obligations is the foundation of any compliant financial system. These rules apply to all businesses operating in Australia and cover registration, calculation, reporting, and documentation.

1. Who must register for GST

Any business with an annual GST turnover of $75,000 or more must register. The threshold for non-profits is $150,000. Turnover refers to gross income, not net profit. A business with high overheads can breach the threshold before generating real profit. Once your projected turnover reaches $75,000, you must register within 21 days.

Ride-sourcing drivers such as Uber must register for GST regardless of their annual turnover. Businesses below the threshold may register voluntarily to claim input tax credits on business purchases and capital investments.

2. How GST is calculated and remitted

For taxable sales, GST equals 10% of the supply value. If a price includes GST, apply the 1/11th rule to find the tax component.

For example, a product sold for $110 inclusive of GST contains a $10 tax component ($110 / 11) and a pre-tax value of $100.

Remittance works on a net basis, supporting proper financial flow management. Businesses deduct GST credits from GST collected and pay the difference to the ATO each period.

GST collected belongs to the ATO. Using these funds for operational cash flow is a serious compliance risk. Keep a separate bank account for GST liabilities and transfer collected amounts regularly to ensure funds are available at lodgment.

3. BAS reporting and lodgment rules

The BAS is the primary vehicle for reporting GST to the ATO. Lodgment frequency is based on annual GST turnover.

Businesses with a structured approach to Australian BAS compliance can better manage reporting timelines, reduce errors, and maintain consistency across reporting periods.

Most SMEs with a turnover below $20 million lodge quarterly. Due dates are on the 28th of the month after each quarter.

Voluntarily registered businesses with a turnover below $75,000 may opt for annual BAS reporting, aligned with their tax return.

The ATO’s Simpler BAS initiative reduces reporting to three labels for businesses under $10 million: total sales, GST collected, and GST paid.

4. GST documentation requirements

For any business purchase over $82.50 (including GST), you must hold a valid tax invoice when lodging your BAS to claim GST credits. If requested, the supplier must provide the tax invoice within 28 days.

A valid tax invoice must include the supplier’s ABN, issue date, item description, GST amount, and the seller’s identity. For purchases of $1,000 or more, the buyer’s ABN or identity must also appear on the invoice.

All records, including invoices, receipts, and calculation workings, must be retained for a minimum of five years.

A structured and regulatory compliant financial system helps ensure these obligations are consistently met while reducing the risk of reporting errors and penalties.

How to Build a GST Compliance Framework

A structured approach is the most reliable way to move from a reactive, error-prone process to a consistent and defensible compliance system.

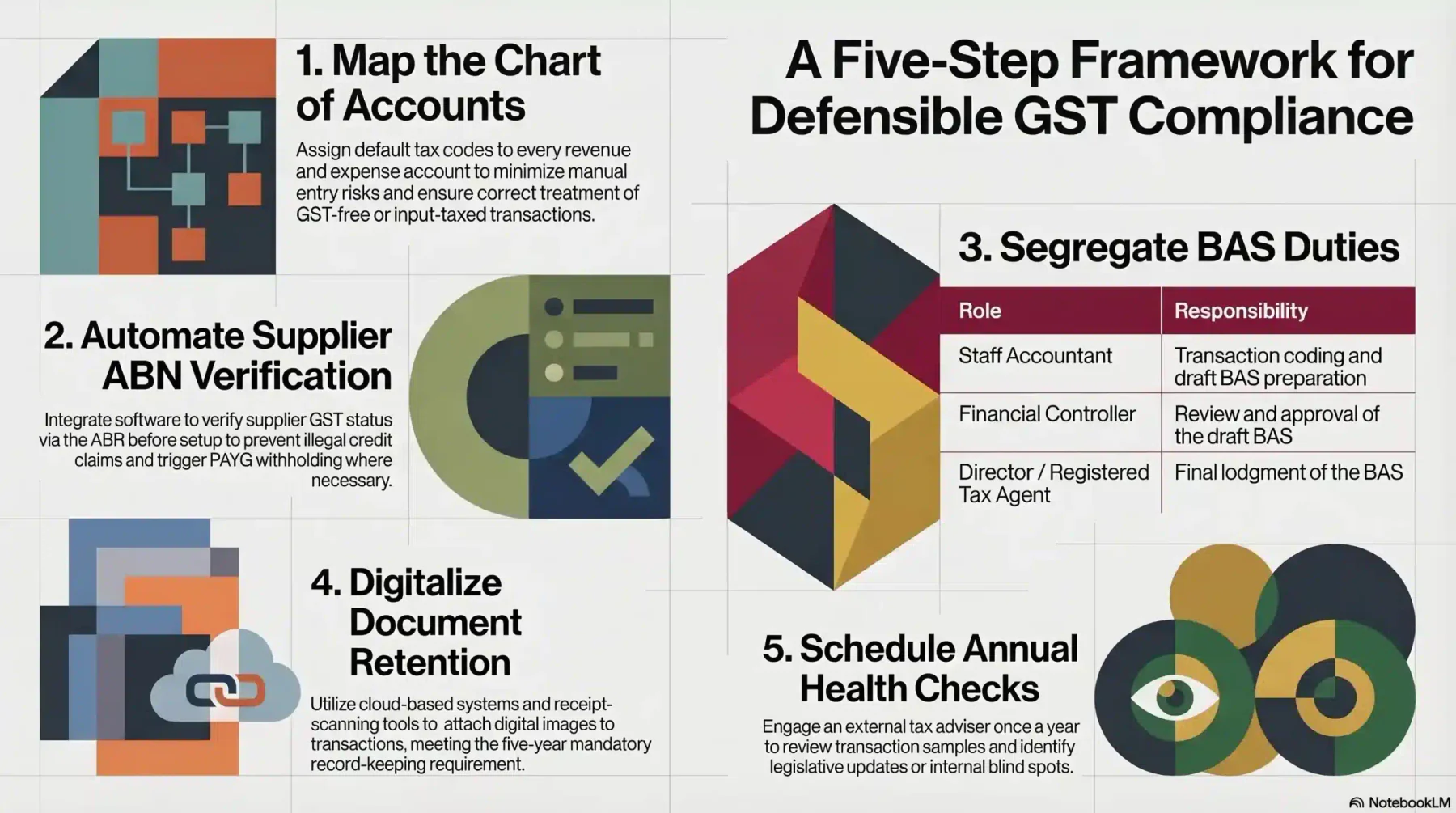

1. Map your chart of accounts

Review every revenue and expense account in the general ledger and assign a default tax code to accounts, minimising manual code selection and reducing risks of miscoding taxable, GST-free, and input-taxed transactions.

This process is more efficient when supported by an accounting platform for Australian businesses that standardises tax treatment across all transactions.

2. Automate supplier ABN verification

Claiming input tax credits from suppliers not registered for GST is a primary trigger for ATO penalties. Use software integrations to verify a supplier’s ABN and GST status via the ABR before setup.

If a supplier is not GST-registered, your system should automatically block credit claims on their invoices and flag the need to withhold PAYG tax where no ABN is provided.

3. Segregate duties for BAS preparation

To prevent errors and fraud, separate the responsibilities of transaction coding, BAS preparation, and final lodgment across different personnel.

A sound workflow assigns the staff accountant to prepare the draft BAS, the financial controller to review and approve it, and an authorised director or registered tax agent to lodge it.

4. Digitalise and centralise document retention

The ATO requires all tax records to be kept for a minimum of five years. Relying on paper receipts or decentralised email folders is a serious audit risk.

Implement a cloud-based document management system and mandate the use of receipt-scanning tools that attach digital images directly to transactions in your accounting software.

5. Schedule regular compliance health checks

Even the best internal systems can develop blind spots. Schedule an independent GST health check at least once a year with an external tax adviser.

The adviser should review a sample of transactions, assess your tax control framework, and identify any legislative updates your internal team may have missed.

GST Compliance Across Industries

While the core GST rules apply universally, their practical application varies significantly across industries. Understanding the nuances of your sector is critical to avoiding misclassification.

1. E-commerce and retail

Australian e-commerce businesses face specific compliance challenges under the Low Value Imported Goods (LVIG) rules.

If your business imports goods valued at $1,000 or less directly to Australian consumers and your global turnover meets the $75,000 threshold, you must register, collect, and remit GST.

Selling digital products to overseas consumers is generally GST-free, provided specific ATO criteria are met. Retailers must configure their systems to apply the correct tax treatment based on customer location.

2. Property and construction

Property and construction businesses face some of the most complex GST rules in Australia. A key example is the Margin Scheme for new residential developments.

Under this scheme, developers calculate GST on the value added (the margin) rather than the full selling price, requiring precise historical valuations and contractual agreements.

For mixed-use developments with both commercial and residential components, businesses must apply rigorous apportionment to claim the correct percentage of input tax credits.

3. Healthcare and medical professionals

Most medical services provided by a recognised professional for patient treatment are GST-free. However, mixed practices require careful revenue segregation.

For example, a chiropractic clinic may provide GST-free adjustments but also sell taxable ergonomic products. Each revenue stream must be coded separately in the billing system.

Medical reports generated for insurance companies or legal proceedings attract the standard 10% GST, unlike reports produced for patient treatment purposes.

4. Information technology and SaaS

Australian IT firms and SaaS providers frequently work with international clients. Services provided to non-residents located outside Australia are generally GST-free exports.

However, if the overseas client has an Australian presence or the service relates to property located in Australia, the GST-free treatment no longer applies.

IT businesses must retain documentation proving the non-resident status and physical location of overseas clients to substantiate GST-free export claims.

Common GST Compliance Mistakes to Avoid

Even well-managed businesses fall into compliance traps due to the complexity of GST legislation and the pace of daily operations. Awareness of these mistakes is your first line of defence.

1. Incorrect GST classification

Not all goods and services sold in Australia attract the 10% tax. Misclassifying GST-free or input-taxed supplies as taxable, or vice versa, leads to significant overpayments or underpayments.

GST-free supplies include basic food, certain medical services, education, and exports. Businesses can still claim input tax credits on costs incurred in making GST-free supplies.

The distinction is not always obvious. Fresh bread is GST-free, but a hot bakery item intended for immediate consumption is taxable. Each product line must be assessed individually.

2. The entertainment expense trap

Many businesses incorrectly assume that client lunches or staff events automatically qualify for an input tax credit.

In reality, the GST treatment of entertainment is tied to Fringe Benefits Tax (FBT). If an expense is exempt from FBT, you generally cannot claim the GST credit on it.

Businesses should document attendees and the purpose of each entertainment expense so accountants can apply the correct tax treatment at the end of the FBT year.

3. Incorrect treatment of motor vehicles

Purchasing a company vehicle involves a GST credit cap. The ATO limits the maximum GST claimable on a passenger vehicle to 1/11th of the car limit, not 10% of the full purchase price.

If the vehicle is used for both business and private purposes, input tax credits must be apportioned based on a valid logbook. Claiming 100% of credits without a logbook is a guaranteed audit trigger.

4. Failing to apportion for private use

The obligation to apportion applies beyond motor vehicles. Mobile phones, home internet, and travel expenses must all be split between business and personal use.

Sole traders and partners are especially at risk. A laptop used 70% for business entitles the owner to claim only 70% of the input tax credits. Usage percentages must be documented and reviewed annually.

5. Relying on invalid tax invoices

To claim an input tax credit for a purchase over $82.50 (including GST), you must hold a valid tax invoice, not just a standard receipt or order confirmation.

A valid invoice must include the supplier’s ABN, issue date, item description, and GST amount. For purchases over $1,000, the buyer’s ABN is also required.

6. Mishandling intercompany transactions

Businesses operating under a group structure must understand whether their entities form a consolidated GST group. Transactions within a GST group are generally disregarded for tax purposes.

If entities are not grouped, standard GST rules apply, and tax invoices must be raised for all intercompany charges, including management fees and administrative recharges.

Best Practices for GST Compliance Management

Maintaining strong GST compliance requires more than meeting minimum obligations. The following practices help businesses build a proactive, well-documented compliance framework.

1. Adopt the ATO’s justified trust methodology

The ATO’s Justified Trust framework requires businesses to provide objective evidence that their tax outcomes are correct, not just assertions of compliance.

To align with this approach, establish a documented tax control framework that defines who makes GST decisions, how those decisions are made, and how data integrity is maintained.

Proactively adopting Justified Trust principles reduces the likelihood of intrusive audits and signals strong governance to lenders and stakeholders.

2. Implement continuous transaction controls and e-invoicing

Australia is transitioning to mandatory e-invoicing via the Peppol network. Forward-thinking businesses are adopting this technology now to stay ahead of the requirement.

E-invoicing enables the direct, secure exchange of invoices between accounting systems, eliminating manual data entry and ensuring tax codes are mapped correctly at the source.

3. Use automated data analytics and exception reporting

Automated exception reporting allows businesses to run continuous checks across 100% of transactional data, rather than relying on manual sampling.

These tools flag anomalies such as missing ABNs, invoices where the GST does not equal 1/11th of the total price, or duplicate payments. Errors are caught before they reach the BAS.

4. Leverage accounting software for end-to-end GST management

Integrated accounting software automates tax code assignment, input tax credit tracking, and BAS preparation, significantly reducing the risk of manual errors.

Using a robust financial reporting system alongside automation tools ensures data accuracy, real-time visibility, and audit-ready compliance records.

Conclusion

GST compliance is an ongoing responsibility for Australian businesses. Businesses that manage GST most effectively treat compliance as a core operational function, supported by documentation, reviews, and proper accounting tools.

From understanding registration thresholds and BAS lodgment rules to avoiding common pitfalls and implementing robust controls, each measure reduces your exposure to ATO penalties and audits.

If you too are interested in complying with GST even further, you can start a free consultation with us and let us lend our guidance to aid your efforts.

Frequently Asked Question

The ATO applies a Failure to Lodge (FTL) penalty based on your business size. Penalties accrue per 28-day period until you lodge, and interest compounds daily on any unpaid amounts.

In some cases, yes. If you register voluntarily and acquire assets for a creditable business purpose before registration, you may be able to claim credits on your first BAS. Confirm eligibility with a registered tax agent.

GST-free supplies (such as basic food) do not attract GST but still allow you to claim input tax credits on related costs. Input-taxed supplies (such as financial services) also carry no GST but don't allow input tax credit claims on related expenses.

GST and VAT are effectively the same type of tax. Both are broad-based consumption taxes applied at each stage of the supply chain, with businesses claiming tax credits paid on inputs. Australia calls it GST, while most of Europe and other countries uses VAT.

Exports of goods and certain services to overseas clients are generally GST-free, provided the goods have left Australia or the recipient is a non-resident without an Australian presence, but you should always try to verify the ATO criteria.