Most Australian businesses that run into cash flow trouble are not short on revenue. The gap is between what was planned and what actually happened, and it often stays invisible until EOFY.

ASIC’s annual reports link poor financial controls to business failures across the country. Quarterly BAS deadlines and PAYG instalment obligations throughout the year mean reactive spending management carries real compliance risk.

Budget reporting compares planned figures against actual results. This article covers how it works, what to include, and how Australian businesses can use it to improve financial control and compliance readiness.

Key Takeaways

Budget reporting compares planned budgets with actual income and expenses to track financial performance and control spending.

The key distinction between a budget report and a financial report lies in their purpose: one measures performance against targets, the other records completed transactions.

Australian businesses rely on budget reporting to manage cash flow, meet compliance requirements, and support informed decision-making throughout the financial year.

Different budget report formats serve different purposes, from operational and capital budgets to cash flow and department-level reports.

What Is Budget Reporting?

Budget reporting is the process of comparing actual financial performance against a projected budget over a specific period. It tracks revenues, expenses, and cash flow to help businesses and individuals identify spending gaps, allocate resources efficiently, and adjust strategies to meet their financial goals.

A budgeting report compares a company’s planned budget with its actual income and expenses over a certain period. It helps businesses see if they are meeting financial goals and staying within budget.

The report shows any differences between expected and actual results, known as variances. This makes it easier to spot overspending, lower revenue, or areas that need attention.

Budgeting reports can cover the whole business or specific departments and projects. They give clear financial insights through an accounting system for budget reports so managers can make better decisions.

Key Components of a Budget Report

A budget report compares planned financial targets with actual results. To make the report useful for decision-making, it should include several core components that provide context for financial performance.

- Budget (Planned): The estimated income or expenses established during the budgeting process. This serves as the benchmark for measuring actual performance.

- Actual Results: The revenue earned or expenses incurred during the reporting period. These figures show how the business performed compared to its original plan.

- Variance: The difference between budgeted and actual figures, usually presented in both dollar value and percentage. Variance analysis helps identify areas that require attention or corrective action.

- Commentary and Action Items: Explanations for significant variances, along with recommended actions or next steps. This provides context behind the numbers and supports better decision-making.

Budget Report vs Financial Report

Budget reports and financial reports both use financial data, but they have different purposes. Financial reports show past performance, while budget reports compare planned budgets with actual results.

Financial reports, including the Profit and Loss (P&L) statement, balance sheet, and cash flow statement, are often shared with investors, regulators, or lenders, so they must follow accounting standards. Budget reports are mainly used internally by managers and business owners.

Financial reports use actual figures only. Budget reports are more flexible and may include forecasts, variances, and custom categories.

Why Budget Reporting Matters for Australian Businesses

Budget reporting helps companies stay financially prepared, meet compliance requirements, and make better decisions with Australian financial reporting software. Budget reporting helps businesses compare actual results with planned targets on a monthly or quarterly basis. This allows companies to spot underperformance early, control rising costs, and adjust strategies before issues grow larger. Many Australian businesses must submit BAS reports each quarter and prepare for EOFY reviews. Budget reporting helps forecast tax obligations, manage cash flow, and measure annual performance more accurately. Investors, directors, and lenders often need clear financial updates. Regular budget reports improve transparency, support better governance, and help businesses maintain access to funding. Businesses often use different budget reports to monitor specific areas of performance. Each report provides useful insights that help improve planning, spending control, and decision-making. This report tracks daily business income and expenses such as sales, payroll, rent, and utilities. It helps management measure whether normal operations are profitable. A capital budget report focuses on long-term investments like equipment, vehicles, property, or system upgrades. It helps businesses control spending on major purchases and avoid budget overruns. This report monitors money coming in and out of the business. It helps ensure there is enough cash available to cover bills, payroll, and short-term obligations. A departmental budget report breaks spending down by teams such as marketing, HR, or IT. It improves accountability by helping managers control their own budgets. This report tracks income and expenses for a specific project. It helps businesses monitor costs, manage timelines, and protect project profitability. A revenue budget report compares actual sales with revenue targets. It helps businesses evaluate sales performance and identify growth opportunities. This report reviews financial performance every three months and often aligns with BAS reporting periods in Australia. It helps businesses track trends and prepare for tax obligations. An EOFY budget summary gives a full-year view of planned budgets versus final results. It supports annual reviews, future planning, and next year’s budgeting process. For quick reference, the table below summarises which budget report fits which business question. A budget report is most effective when it includes clear, relevant, and actionable information. The right structure helps businesses understand performance, identify issues, and create a comprehensive financial report for better decision-making. This section compares planned amounts with actual income or expenses for each category. It helps businesses quickly see where results are on track or off target. Variance analysis shows the difference between budgeted and actual figures in both dollar value and percentage. This makes it easier to measure the size and impact of financial gaps. This section explains why major variances happened and what factors caused them. Clear commentary gives context to the numbers and supports better decision-making. A forward-looking forecast estimates financial performance for the rest of the reporting period. It helps management plan ahead and adjust budgets when needed. This part lists the steps needed to fix issues or improve results. Assigning owners and deadlines creates accountability and ensures follow-up action. Australian businesses operate within a regulatory framework that shapes how budget reporting must be structured and timed. Meeting these requirements supports compliance, improves stakeholder confidence, and reduces financial risk at year-end. The AASB sets the standards for preparing and presenting financial information in Australia, including AASB 1055. This standard requires government and public sector entities to disclose budget information alongside financial statements to support public accountability. Budget reports that follow these classifications also support the preparation of audited financial statements for large proprietary companies. When internal budget data uses the same account structure as AASB-compliant statements, reconciliation between management reports and audited financials becomes faster and less error-prone. This reduces preparation time and minimises discrepancies during the audit process. Australian businesses registered for GST must lodge a BAS each quarter. Budget vs actual variance analysis helps finance teams forecast GST liability and PAYG instalment obligations before each lodgement date, rather than calculating them under time pressure. Separating GST-applicable items from non-taxable ones within the budget report improves cash flow forecasting accuracy. This reduces the risk of underpaying PAYG instalments and incurring ATO penalty interest across the financial year. At the end of the financial year on 30 June, Australian businesses reconcile the full-year budget against actual results. This annual review is standard for boards, ASIC-reporting entities, and any business subject to external oversight. Lenders commonly request budget-to-actual comparisons during annual covenant reviews or credit facility renewals. A consistent budget reporting process ensures this documentation is ready when needed, rather than compiled under deadline pressure. Creating budget reports manually can take time and increase the risk of errors. Using ready-made templates helps standardize reporting, improve accuracy, and save time across financial periods. This template is used to track monthly revenue and operating expenses. It gives a clear view of current performance and year-to-date progress. TEMPLATE MONTHLY REPORT A capital budget template helps monitor spending on major assets or long-term projects. It compares approved budgets with actual costs and remaining funds. TEMPLATE CAPITAL BUDGET REPORT This template tracks cash coming in and going out of the business. It helps businesses monitor liquidity and maintain a healthy cash position. TEMPLATE CASHFLOW BUDGET REPORT A departmental budget template shows each team’s allocated budget and actual spending. It helps managers control costs and stay within budget limits. TEMPLATE DEPARTMENTAL BUDGET REPORT Creating a budget report becomes easier when you follow a clear and structured process. These steps help ensure your report is accurate, useful, and actionable for decision-makers. Start by identifying why the report is needed and who will use it. This helps determine the level of detail, reporting period, and format required. Use approved budgets or financial plans as the starting benchmark. A clear baseline ensures actual results can be measured accurately and supports effective budget planning. Gather real financial data from accounting systems, invoices, or reports. Check for errors or missing entries before preparing the report. Compare actual figures against the budget to find differences. Focus on major gaps that may affect business performance or spending control. Explain key variances, include updated forecasts, and suggest actions. This turns financial data into insights management can use. Share the report with relevant stakeholders and assign responsibilities. Following up ensures decisions are acted on and progress is monitored. Applying consistent practices makes budget reports more accurate, more actionable, and easier to maintain across reporting periods. The four practices below reflect what well-run finance teams in Australia do consistently. The Australian financial year runs from 1 July to 30 June. Aligning budget reports to this cycle keeps reporting consistent with BAS lodgement periods and EOFY financial statements. Monthly or quarterly reporting timed to this calendar avoids reconciliation across different reporting windows and reduces discrepancies when preparing year-end accounts. Not every variance requires management attention. Setting materiality thresholds, such as flagging differences above 5% or a set dollar amount, keeps reports focused on issues that genuinely affect business performance. Without thresholds, reports fill with minor discrepancies that distract from significant trends. Defining these limits upfront also standardises the review process across departments and reporting periods. A budget set at the start of the year becomes outdated as conditions change. Pairing monthly budget reports with rolling forecast updates keeps projections current and gives management a realistic view of where performance is heading. Rolling forecasts incorporate recent actuals and revised assumptions rather than relying on figures set months earlier. This supports faster decisions and reduces the risk of missing key financial targets. When budget data and actual figures live in different systems, reconciliation takes time and errors accumulate. Connecting it to an accounting system for budget reports like HashMicro creates a single source of truth where planned figures and actuals sit in the same environment. This integration removes manual data transfers and reduces duplicate entry errors. Finance teams gain real-time visibility into performance and can generate reports on demand rather than waiting for end-of-period data collection. Budget reporting helps businesses compare planned budgets with actual financial results. It gives clear insights into revenue, expenses, and overall performance. Regular budget reports help companies control costs, identify issues early, and make better financial decisions. They also improve accountability across departments and teams. For Australian businesses, budget reporting supports BAS preparation, EOFY reviews, and future planning. Using the right systems and templates can make reporting faster and more accurate. Consult with our experts to discover how smarter budget reporting can improve financial control, accuracy, and business performance. A budget report compares planned budgets with actual income and expenses. It helps businesses track financial performance. It helps businesses control costs, find problems early, and make better decisions. Most businesses prepare budget reports monthly or quarterly, depending on their needs. A budget report should include budget figures, actual results, variances, and forecasts.1. Tracking financial performance against the business plan

2. Supporting BAS quarterly and EOFY budget reviews

3. Meeting stakeholder, board, and lender reporting obligations

Types of Budget Reports

1. Operating budget report

2. Capital budget report

3. Cash flow budget report

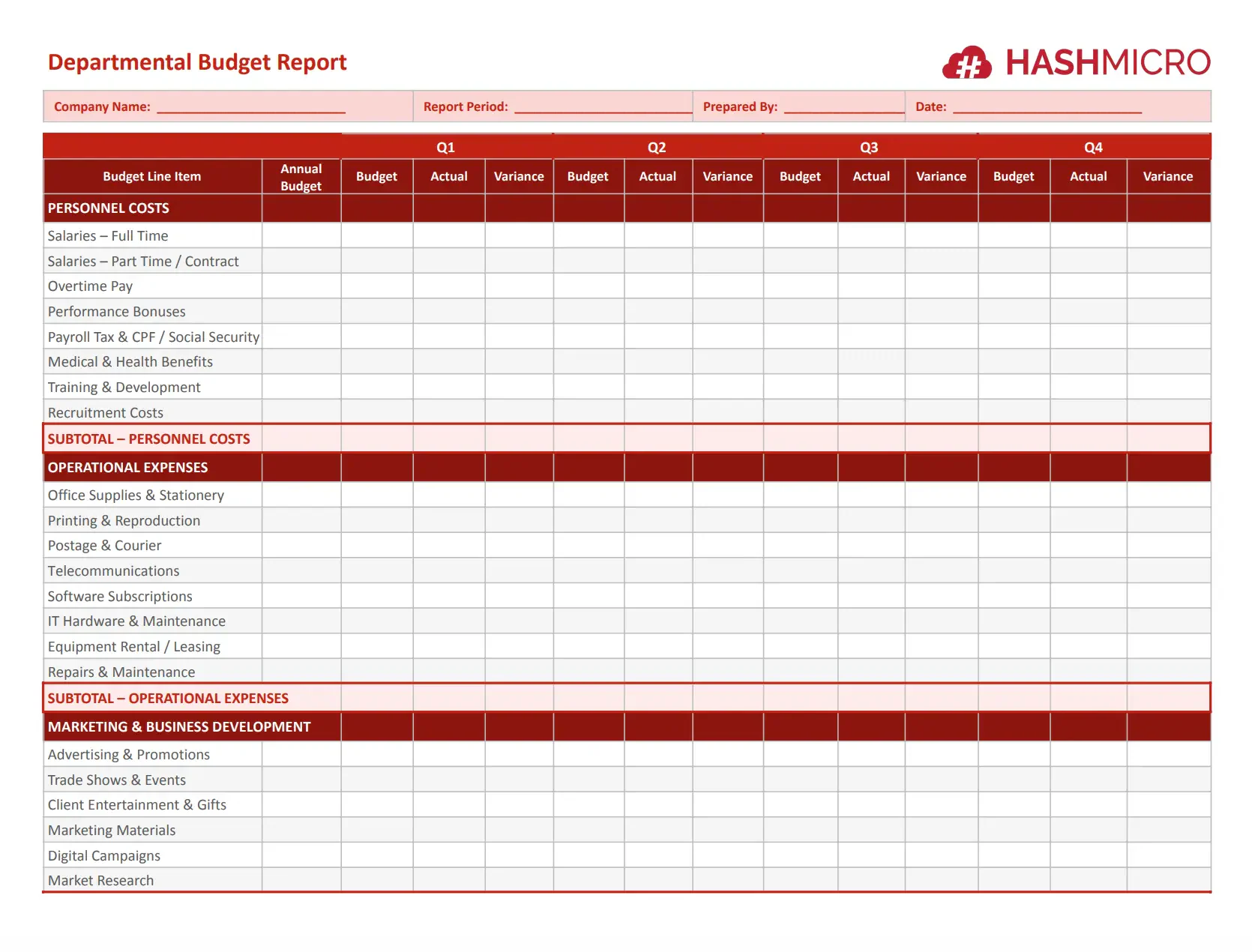

4. Departmental budget report

5. Project budget report

6. Revenue budget report

7. Quarterly budget report

8. EOFY annual budget summary report

Report Type

Business Question Answered

Best Used By

Typical Frequency

Operating budget report

Are daily operations generating profit?

Finance managers, department heads

Monthly

Capital budget report

Are major investments staying within approved limits?

CFOs, project managers

Quarterly or per project

Cash flow budget report

Do we have enough cash to meet upcoming obligations?

Finance teams, business owners

Monthly or weekly

Departmental budget report

Is each team spending within its allocation?

Department managers, HR

Monthly

Project budget report

Is this project on budget and on schedule?

Project managers, finance teams

Per project milestone

Revenue budget report

Are we hitting our sales targets?

Sales managers, finance teams

Monthly or quarterly

Quarterly budget report

How did the business perform this quarter?

Management, boards, BAS preparation teams

Quarterly

EOFY annual budget summary

Did we meet our full-year financial goals?

Boards, lenders, ASIC-reporting entities

Annually

What to Include in a Budget Report

1. Budget vs actual figures by category

2. Variance analysis, dollar amount and percentage

3. Key assumptions, drivers, and commentary

4. Forecast for the remaining period

5. Action items and responsible owners

Australian Regulatory Context for Budget Reporting

1. AASB and corporate reporting alignment

2. ATO and BAS quarterly preparation

3. EOFY budget review and lender obligations

Download Free Budget Reporting Templates

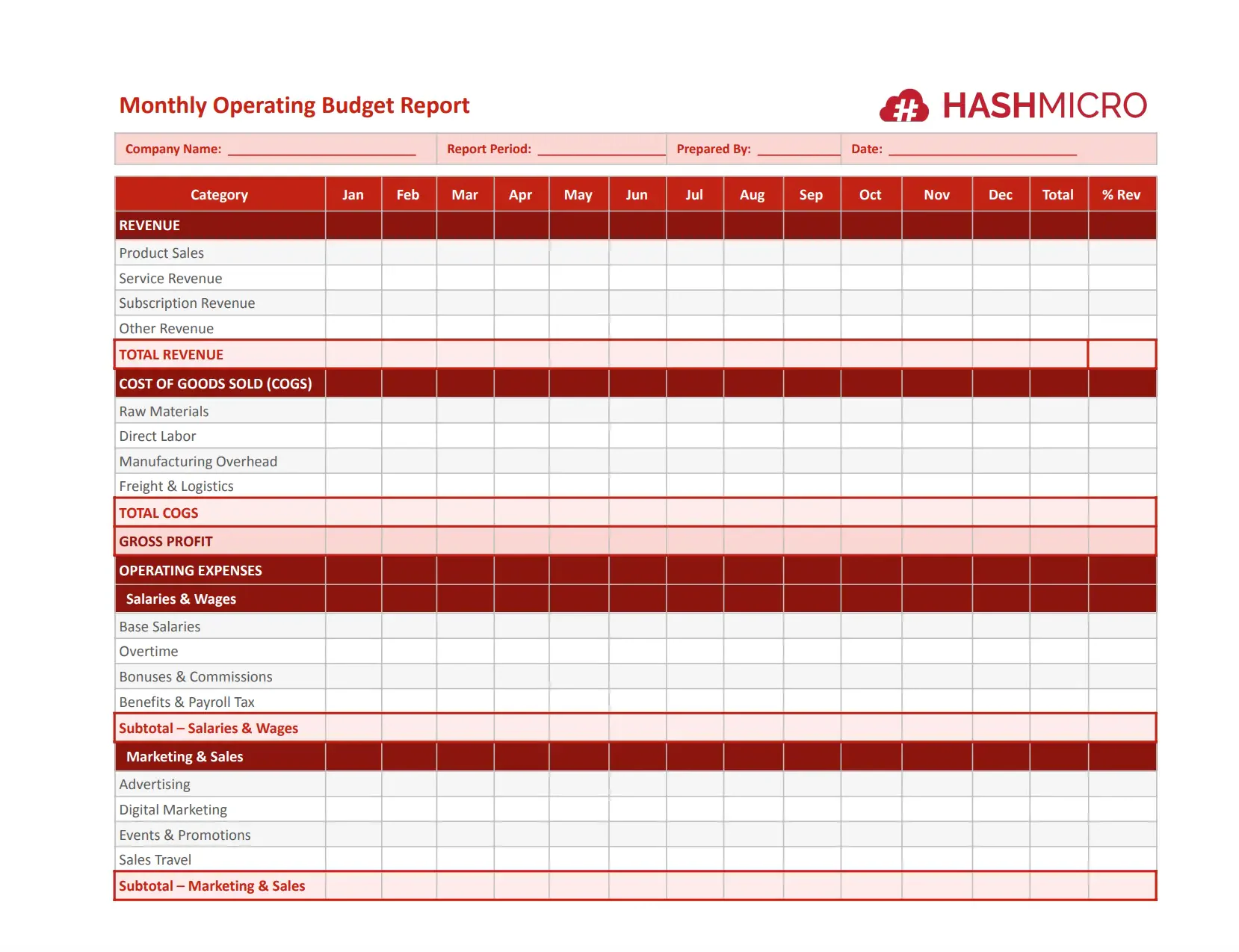

1. Monthly operating budget report template

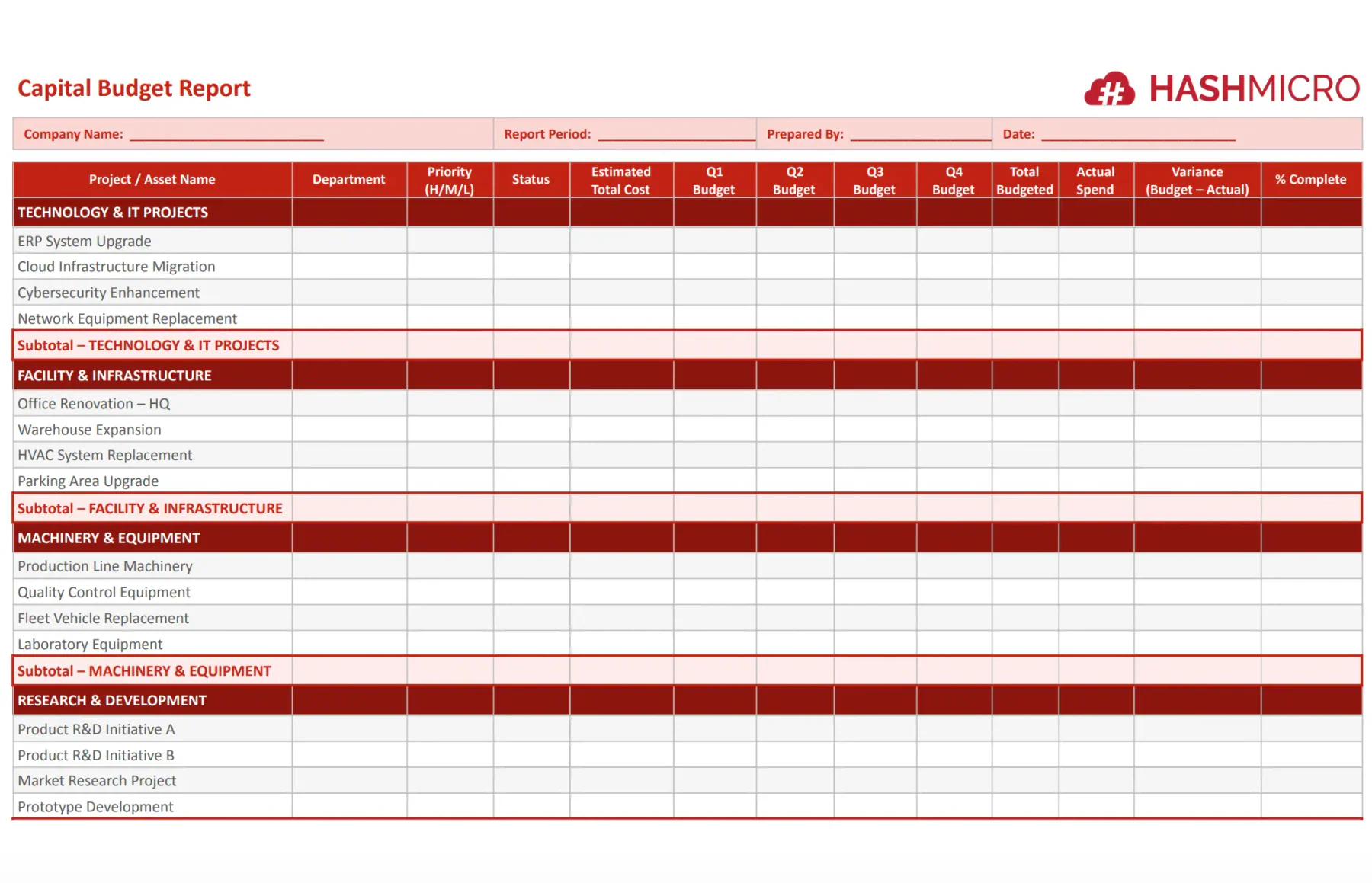

2. Capital budget report template

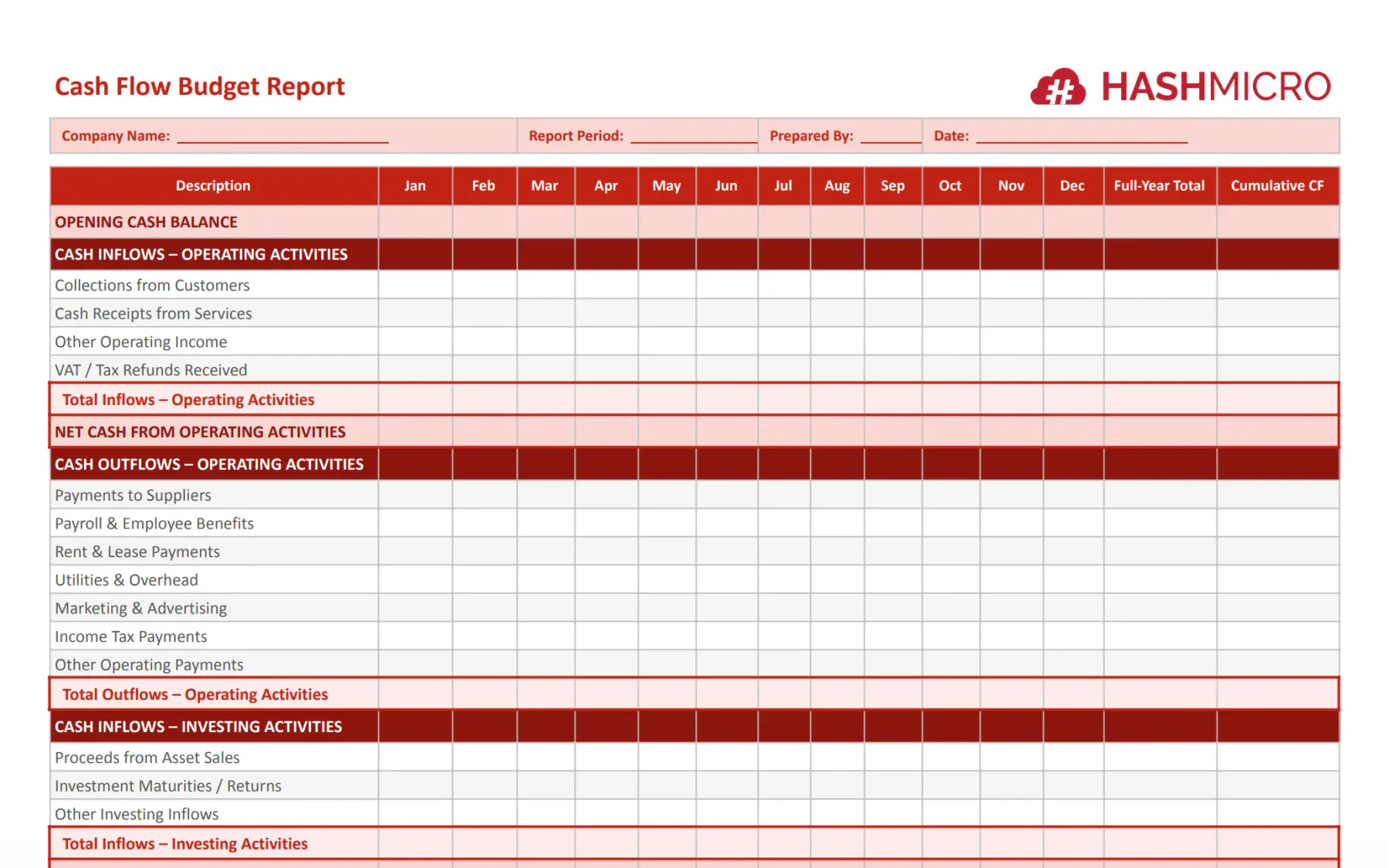

3. Cash flow budget report template

4. Departmental budget report template

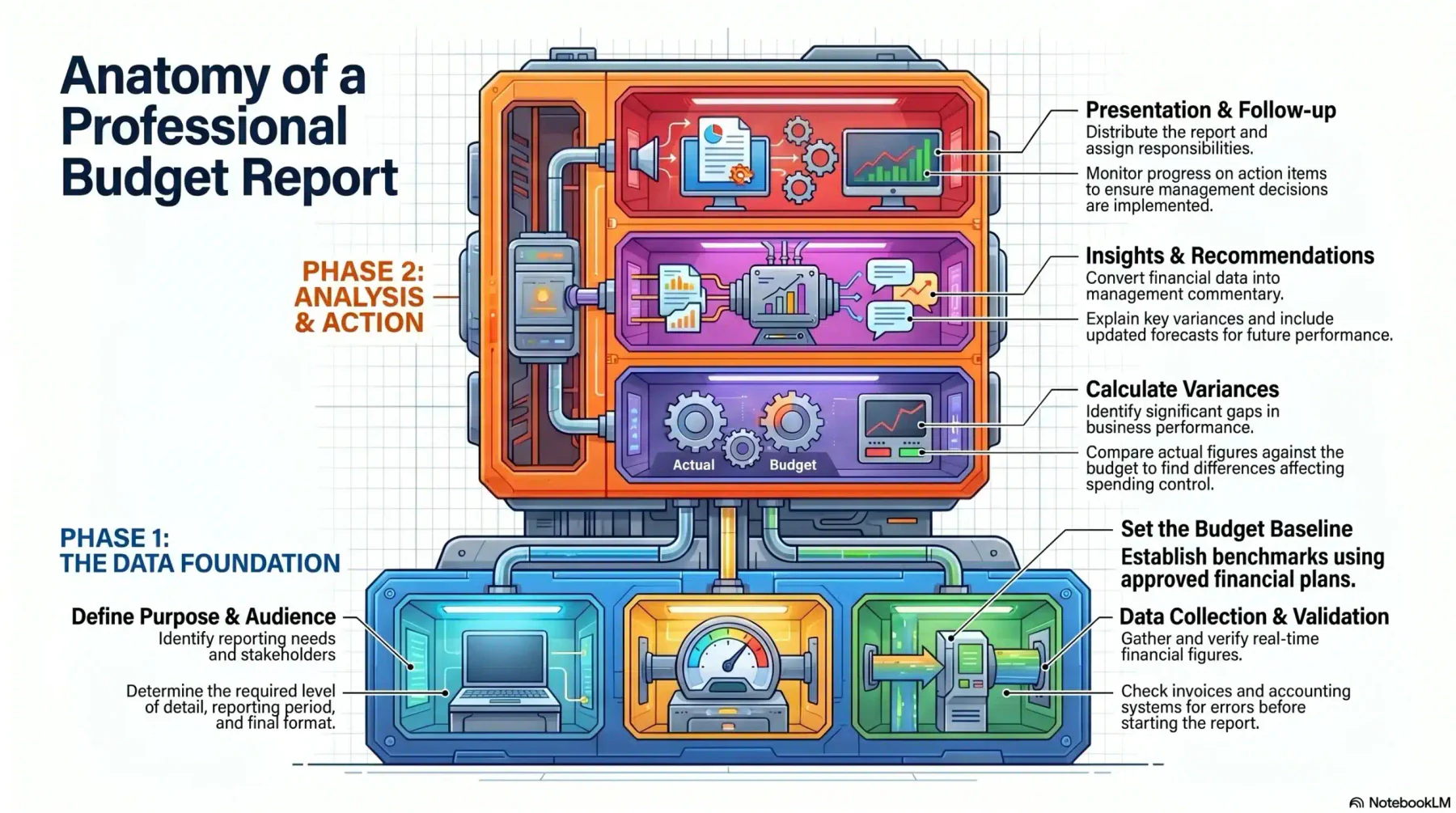

How to Create a Budget Report Step by Step

1. Define the report’s purpose and audience

2. Set your budget baseline

3. Collect and validate actual financial data

4. Calculate variances and identify significant gaps

5. Write commentary, forecasts, and recommendations

6. Present, distribute, and follow up on action items

Budget Reporting Best Practices for Australian Businesses

1. Time budget reports to the Australian financial year (1 July – 30 June)

2. Build materiality thresholds before flagging variances

3. Pair budget reports with rolling forecast updates monthly

4. Connect budget reporting to ERP for single source of truth

Conclusion

Frequently Asked Question