Every business faces the complex challenge of managing outgoing cash flow effectively. Accounts payable represent a fundamental pillar of finance that dictates overall financial health.

Business leaders must understand this function thoroughly to maintain strong vendor relationships and ensure long-term operational stability. Failing to manage accounts payable properly will surely bring unwanted risks to your company and potentially ruin relationships with partners and suppliers.

The importance of understanding accounts payable is a vital and fundamental part of business. This blog will elaborate on every important detail you need to know about accounts payable, and even additional information that all businesses in Australia must know.

Key Takeaways

Understand the fundamental definition of accounts payable and its role as a short-term liability.

Explore how accounts payable works through a comprehensive seven-step procure-to-pay process.

Discover the differences between accounts payable and account receivable to balance incoming and outgoing cash.

Learn about things to consider when managing accounts payable regarding local tax compliance.

What is Accounts Payable?

Accounts payable (AP) is the short-term debt a company owes to its suppliers or vendors for goods and services received on credit. This financial obligation appears as a current liability on the corporate balance sheet. Businesses must settle these debts within a specified timeframe to maintain their credibility.

Managing these liabilities requires a delicate balance between preserving cash and fulfilling vendor agreements. Delaying payments too long can damage supplier relationships and result in late fees, while paying invoices too fast can drain cash reserves that the business might need for unexpected cash needs.

Analysts closely monitor the accounts payable turnover ratio to evaluate liquidity and operational efficiency. A high turnover ratio indicates quick payments to suppliers and responsible debt management. A low ratio might suggest cash flow problems or a strategic decision to hold onto cash for longer periods.

AP serves as vital control over corporate spending and fraud prevention. Accurate payable data is needed to forecast cash requirements and make informed decisions. Accurate data ensures a truthful picture of your company’s financial health to external stakeholders.

How Accounts Payable Works

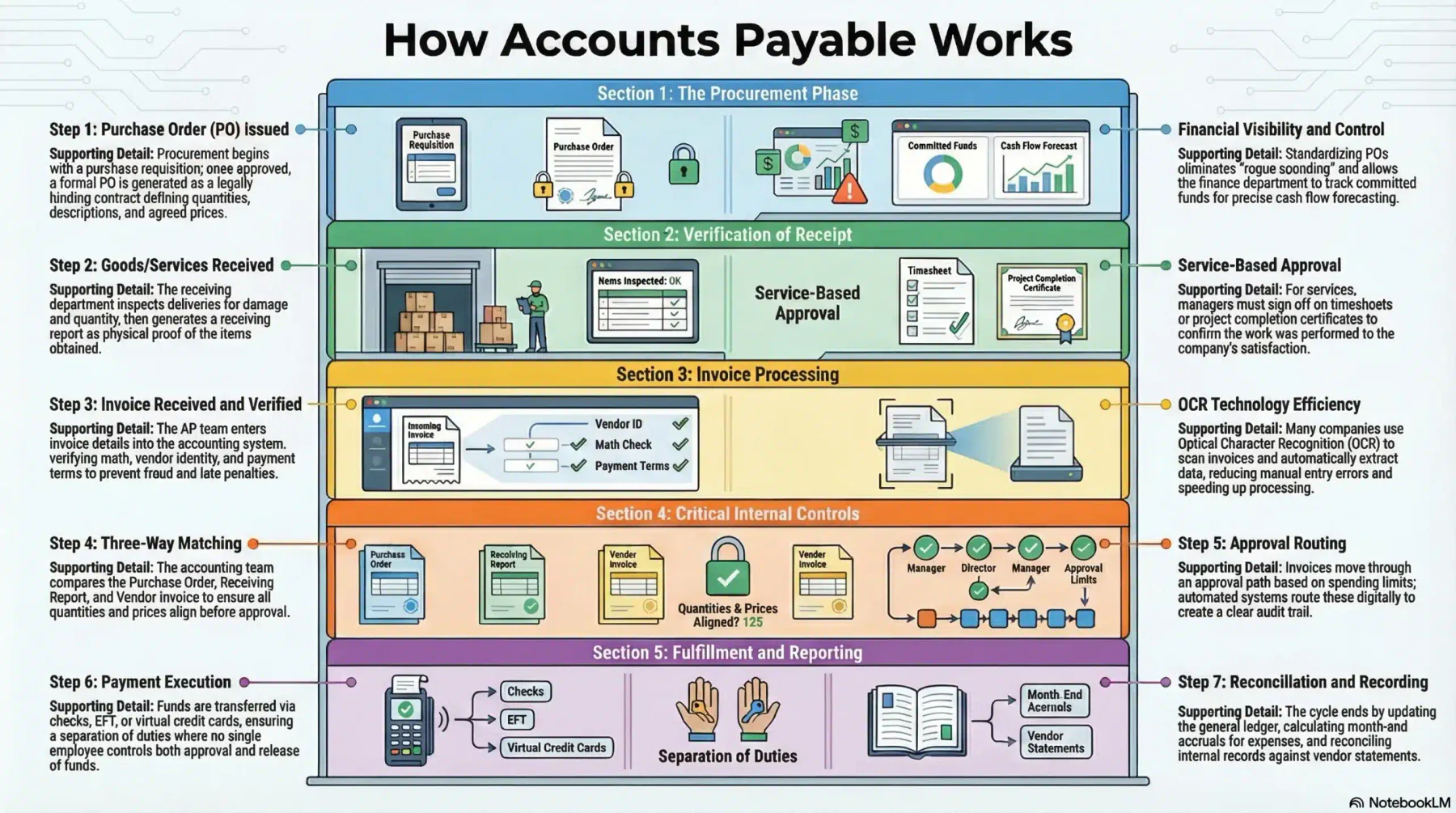

The accounts payable process encompasses a series of coordinated steps known as the procure-to-pay cycle. This workflow ensures that your company only pays for goods and services that are actually ordered and received, as it will protects the business from financial inconsistency and internal fraud.

1. Purchase order issued

Procurement begins when a department identifies a specific business need and submits a purchase requisition. After management approves, the purchasing department generates a formal purchase order (PO).

This document outlines the quantities, descriptions, and agreed prices for the requested goods or services. A purchase order serves as a legally binding contract between buyers and vendors, protecting both parties by defining the expectations and terms of the transaction before any work begins.

Vendors rely on this document to prepare their shipments and allocate their internal resources accordingly. Issuing a purchase order also helps the finance department track committed funds before the invoice arrives. This visibility allows cash flow forecasts to be adjusted with high precision.

Without PO, companies risk overspending and losing control over expenses. Standardizing POs processes eliminates rogue spending and unauthorized vendor engagements. This approach allows your company to negotiate better volume discounts and build stronger relationships with suppliers.

2. Goods/services received

The next phase occurs when the vendor delivers the physical goods or completes the requested services. The receiving department takes responsibility for inspecting the delivery to ensure it matches the original order.

Staff members must verify the physical quantities and check for any visible damage during transit. Upon successful inspection, the receiving team generates a receiving report to document the delivery. This internal document serves as proof that the company obtained the items listed on the PO.

The receiving report becomes a vital piece of evidence for the accounting department later in the payment cycle. Handling partial deliveries requires attention to detail from the receiving staff. If a vendor ships only half of the ordered items, the receiving report must clearly state the exact shortage.

Service-based transactions has a slightly different approach to the receiving process. A department manager must sign off on a timesheet or a project completion certificate. This approval confirms that the vendor performed the services to the company’s satisfaction.

3. Invoice received and verified

After goods or services are delivered, the vendor sends an official invoice requesting payment. The accounts payable team receives it and begins a review by entering the invoice details into the accounting system and checking that everything is accurate.

They verify the math, confirm the vendor’s identity against the approved master vendor list, and review the payment terms. This step prevents fraud, avoids late penalties, and lets your company take advantage of early payment discounts when available.

Many companies now use optical character recognition (OCR), a technology that scans invoices and automatically extracts key data. This reduces manual entry errors, speeds up processing, and makes the verification stage far more efficient.

4. Three-way matching (PO vs receipt vs invoice)

5. Approval routing

6. Payment execution

The payment execution phase is when the company actually transfers money to the vendor. The accounts payable team schedules payments based on invoice terms and accurate cash position monitoring to ensure bills are paid on time without slowing liquidity.

Businesses use different payment methods depending on vendor preferences and transaction size. While paper checks are still used in some industries, electronic funds transfers are faster and more secure, and virtual credit cards are increasingly popular because they offer potential cash rebates.

Strong internal controls are critical at this stage. Companies must separate approval and payment responsibilities to prevent fraud, ensuring that no single employee has full control over releasing company funds.

7. Reconciliation and recording

Accounts Payable vs Accounts Receivable: What’s the Difference?

Accounts payable and accounts receivable represent opposite sides of the same transaction. When one company records a payable, the other records a receivable for the exact same amount. Together, these two functions directly impact cash flow, liquidity, and the overall cash conversion cycle.

| Accounts Payable (AP) | Accounts Receivable (AR) | |

| Definition | Money owed to vendors for credit purchases. | Money owed by customers for credit sales. |

| Financial Position | Current liability (future cash outflow). | Current asset (future cash inflow). |

| Main Objective | Manage payments strategically without harming vendor relationships. | Collect payments quickly to support operations. |

| Key Risk | Fraud, duplicate payments, missed discounts. | Bad debt and customer default. |

| Cash Flow Impact | Reduces cash when payments are made. | Increases cash when customers pay. |

Accounts Payable Examples

Accounts Payable for Australian Businesses: Key Considerations

Common Accounts Payable Pitfalls and Mitigation Strategies

- Invoice Discrepancies and Exceptions

- Duplicate Payments and Fraud Risks

Advanced Best Practices for Accounts Payable

- Dynamic Discounting and Supply Chain Finance

- Centralized Master Vendor Data Management

A strong accounts payable process starts with clean and well-managed vendor data. Leading AP teams use centralized master data controls to keep supplier information accurate and up to date.

This includes regularly reviewing vendor records, removing inactive suppliers, merging duplicates, and verifying tax identification numbers. Maintaining an organized vendor database reduces compliance risks, simplifies year-end reporting, and improves the accuracy of spending analysis.

- Continuous Improvement and Spend Analytics

Conclusion

Accounts payable is far more than a routine bill-paying function. It plays a critical role in managing cash flow, protecting profitability, and maintaining strong supplier relationships. When handled strategically, AP strengthens supply chains and supports long-term financial stability.

Frequently Asked Question

Accounts payable is important because it affects cash flow. If managed improperly, your company will risk cash shortages, damaged supplier relationships, and penalties or late fees.

Accounts payable is a liability, not a cost. Expense is recorded when goods or services are used. Accounts payable simply records the unpaid amount owed.

Yes, some companies strategically extend payment timing to manage working capital. However, excessive and unplanned payment delays can lead to improper accounts payable management.

Accounts payable is recorded by debiting the relevant expense or asset account and crediting the accounts payable account when an invoice is received. The payable is cleared once the payment is made to the supplier.

The two main types of accounts payable are trade payables, which relate to goods and services from suppliers, and non-trade payables, such as taxes, utilities, and other operating obligations.